Registering, reporting and paying taxes are obligations that must be obeyed by the public, especially for MSME business owners. In October 2021, the passage of the Tax Regulation Harmonization Law (HPP) policy stated that there was non-taxable income (PTKP) for MSMEs. The type of tax for MSME business owners is income tax or what can be called the Final Income Tax (PPh) for Micro, Small and Medium Enterprises (MSMEs). Provisions of PP Number 23 of 2018 concerning income tax from businesses received by business owners who have a certain gross circulation.

In 2022, the HPP Law has been enacted related to income tax with an annual turnover exceeding Rp. 500,000,000, - so that the Final Income Tax rate for MSMEs can be charged. For MSMEs with an income of less than Rp.500,000,000 a year, there is no need to pay the final income tax of 0.5%. The objectives of issuing Government Regulations (PP) include:

1) Encourage the role of society in formal economic activities

2) Provide convenience in carrying out tax obligations

3) Providing justice for MSMEs

4) As well as providing an opportunity to contribute to the country

The criteria for MSMEs that get a Final Income Tax Tariff Discount include:

- MSMEs that have a gross circulation (turnover) of not more than Rp. 4.8 billion per year which includes trading businesses, services (kiosks and grocery), clothing sellers, electronic goods sellers, restaurants and other businesses.

- Conventional types of MSMEs and MSMEs engaged in online sales that are hawked in marketplaces and social media.

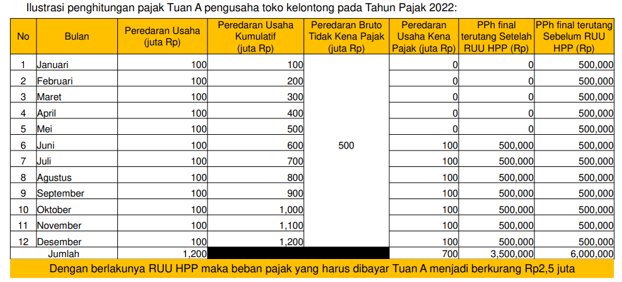

How to calculate the Final Income Tax for MSMEs after the enactment of the HPP Law, namely:

The HPP Law per year 2022 has been enacted with provisions in accordance with the PP, namely MSMEs that have a turnover of more than RP.500,000,000, - in one year will only be subject to the final income tax rate for MSMEs. If the turnover in a year does not reach RP.500,000,000, - then it is not subject to the final income tax of MSMEs.

source : Ministry of Finance, Koinworks.com, smconsult.co.id